Soft Pull vs Hard Pull and When Lenders Should Use Each

Credit bureau data can make or break a lending decision, but understanding how to use it isn’t always straightforward. One of the biggest points of confusion for new and growing lenders is the difference between a soft pull and a hard pull, and how each one shapes risk, cost, and customer experience. Getting this right can streamline underwriting, prevent unnecessary score impact, and strengthen compliance.

Whether you're building your first credit model or integrating bureau checks through SparkLMS, this guide provides a clear and practical breakdown of how soft and hard pulls work as well as their role in modern lending.

Also Read: SparkLMS: Automation Built for Scalable Lending

A credit pull (or credit inquiry) is a request for a borrower’s credit information from bureaus like Experian, TransUnion, or Equifax. Depending on the type of pull, lenders may receive just a credit score or a complete credit file with detailed payment history and risk indicators.

This data helps lenders understand how a borrower has managed credit in the past. A single pull can reveal active loans, past defaults, signs of overextension, bankruptcies, recent loan applications, and potential fraud or identity inconsistencies.

These insights form the foundation of any underwriting model. When this process is integrated through SparkLMS loan management platform, lenders can automate credit pulls across different stages of the loan journey and ensure each inquiry aligns with their risk thresholds and compliance rules.

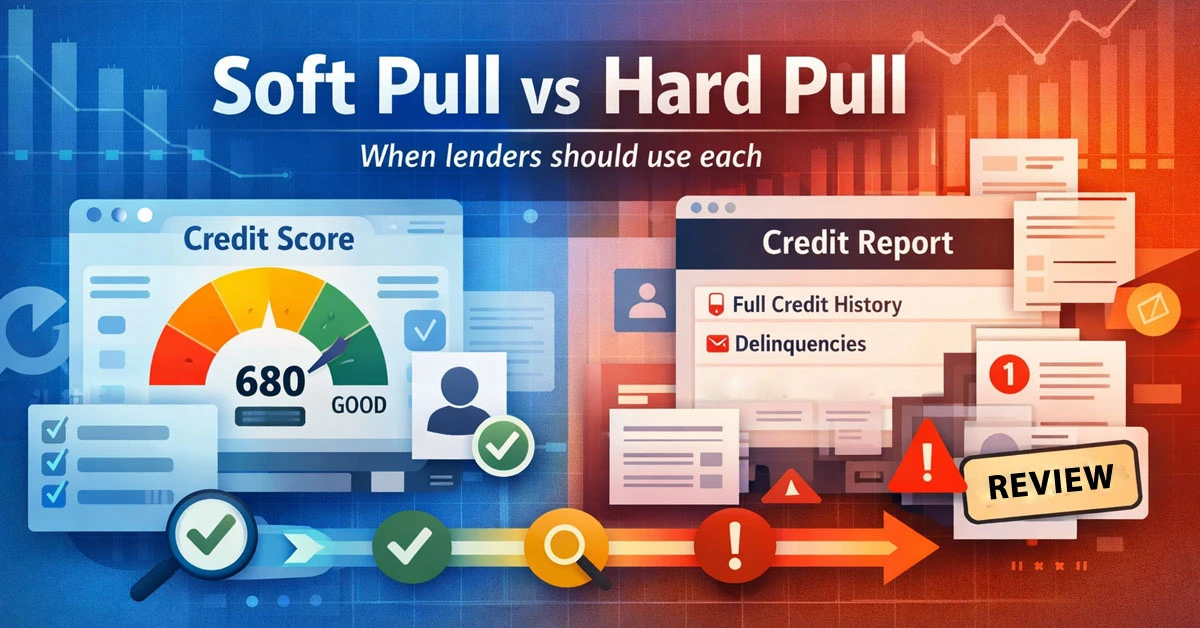

A soft pull is basically a quick peek into someone’s credit profile. It doesn’t impact their score, and borrowers generally feel more comfortable with it because it keeps things low-pressure. Lenders use it when they want to understand the applicant without going all-in on a full credit check.

Soft pulls fit naturally into the early parts of the lending journey, especially when speed matters and you’re trying to avoid unnecessary drop-offs. Lenders often use them for:

Soft pulls help lenders identify red flags early while keeping the application process smooth and borrower-friendly.

A hard pull is applied when underwriting shifts from screening to confirmation. It’s the full-version credit check, the one that does leave a small, temporary mark on the borrower’s credit score. Lenders typically use it only when they’re ready to make a real lending decision, and the borrower is close to accepting terms.

A hard pull pulls back the curtain on the borrower’s entire credit life, including:

In short, it’s the most detailed snapshot a lender can get.

Hard pulls come in when the stakes are higher. Lenders typically use them for:

They take slightly longer, cost more, and require more documentation, but the trade-off is that lenders get the complete risk picture that something soft pulls can’t offer.

| Factor | Soft Pull | Hard Pull |

|---|---|---|

| Impact on Credit Score | No effect on the borrower’s score | Causes a temporary dip and stays on file for up to 24 months |

| Depth of Information | Snapshot-level data (score, open accounts, inquiries, red flags) | Full credit file with complete payment history, utilization, and public records |

| Borrower Consent | Minimal or implied consent | Explicit, documented consent required |

| Cost & Turnaround Time | Lower cost, near-instant | Higher cost, slightly slower |

| Use Case | Pre-qualification, lead filtering, and early risk checks | Final approval, high-value decisions, regulatory checks |

| Best For | Reducing friction and screening high volumes | Validating affordability and confirming borrower eligibility |

Not all lending models treat credit pulls the same way. Subprime, cash-flow-based, and small-dollar lenders often follow a different rhythm because their borrowers and underwriting priorities look different.

For subprime segments, a soft pull is usually the safe starting point because the focus is less on strong credit history and more on spotting risk signals early. Soft pulls help:

Soft pulls help subprime lenders filter quickly without harming borrower confidence.

A hard pull becomes relevant only when the lender needs deeper certainty. Typically, this happens when:

Since every hard pull affects score visibility, subprime lenders use them carefully and only when they improve underwriting accuracy.

SparkLMS streamlines both soft and hard pulls by handling the entire process end-to-end.

SparkLMS helps lenders run smarter, faster, and fully compliant credit checks with zero operational friction.

Soft and hard pulls each serve a clear purpose in the lending journey. Soft pulls keep the early funnel smooth by offering quick, low-impact insights, while hard pulls give lenders the depth they need for confident, compliant approval decisions. Using the right pull at the right stage helps reduce fraud, improve accuracy, and protect both lenders and borrowers.

With SparkLMS, this balance becomes effortless. The platform automates when and how each pull is used, ensuring smarter decisions, cleaner workflows, and a stronger, more reliable underwriting process.

A soft pull can stay on your credit report for up to 12–24 months, depending on the credit bureau. However, it is only visible to you and does not impact your credit score.

No, lenders cannot see soft pulls when reviewing your credit for loan approval. Only you can view them on your credit report, so they don’t affect lending decisions.

No, multiple soft pulls are not bad. They do not affect your credit score and are typically used for pre-approvals or background checks without risk.